(To download a printable pdf of this paper please click here.)

To say a lot has changed in the last three months is an understatement.

In our last white paper, “Don’t Sound the Alarm Until You See the Whites of their Eyes,” we drew the analogy of “wolves” out in the woods that were watching our village and crops. The wolves were geopolitical and market forces that could threaten our safety. The crops and the village, of course, were our investments. Our position was that the wolves must be watched, but we should not take drastic action that could cripple our food source in the long term—rather, we should diligently stay on watch. Not until the wolves were so close we could see the whites of their eyes should we close the gates and do battle, diverting attention and resources from our valuable crops.

A lot changed in three short months.

We’re in a new season. We are slowly emerging from a long, cold, barren COVID-19 winter. Despite the fact it is February, we feel as if we’re in spring because a vaccine is now being distributed. Although the pandemic may get worse before it gets better, there is light on the horizon. The pandemic is a very big, bad wolf that seems to be retreating into its lair, but we must continue to keep our eyes on him.

The wolf of political uncertainty is also gradually retreating. A new administration is in place. We don’t know what this will mean, but it is a wolf we can now see, which allows us to make calculated moves. We must remain vigilant.

Many who watched these wolves but tended their gardens and crops did well. According Barron’s, three major U.S. indexes gained in 2020, despite the significant dip in March. While the Dow rose by 9.7% the S&P 500 was up 18.4% and the Nasdaq by a whopping 45%.

In this, our new season, we are taking the approach that we must continue to watch for new threats, but it is also time to rotate some crops based on what we now know. Here is our position for this quarter.

- We remind ourselves and our clients that markets tend to be leading economic indicators, so what happens in the markets will likely not track with what happens in the economy—rather, it will foreshadow. Following that logic, we can’t depend on lagging economic data as a market indicator.

- Our team assigns a 60% probability of a continued economic recovery, supported by the arrival and approval of vaccines. This and other indicators suggest the importance of staying invested in equities.

- Because of the risk of tech trouble yet potential for strong sector recoveries, we believe it is important to spread risk evenly among equity sectors.

- Relative stock valuations are revealing purchasing opportunities, including dividend stocks. Many of the sectors that were disrupted due to consumer behavior shifts or rapidly changing interest rates may soon be poised for recovery.

- We see continued low yield on fixed income due to low interest rates, driving us away from treasuries and bond funds and toward high-quality, short-term bonds and high-yield municipal bonds.

Why do we recommend staying invested in equities?

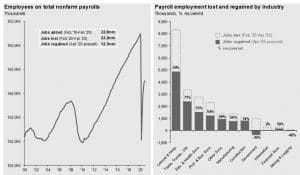

Source: Bureau of Labor Statistics, J.P. Morgan Asset Management Guide to the Markets – U.S. Data as of Dec 31, 2020

As more people become vaccinated against COVID-19, jobs and earnings are projected to grow. In fact, jobs are already on the rebound from their low point.

Source: Bureau of Labor Statistics, J.P. Morgan Asset Management Guide to the Markets – U.S. Data as of Dec 31, 2020

The consumer balance sheet is stronger than it has been in decades, and consumer spending accounts for 68% of the GDP. With money in their pockets, we believe consumers will express their pent-up demand for certain good and services as they feel more comfortable.

Source: BLS, FactSet, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of December 31, 2020.

There are strong reasons to believe interest rates will stay low for some time. We believe this because the Fed has said as much. This chart was prepared by the U.S. Federal Reserve based on the stated policies and conversations of the 17-member Federal Reserve Board. This bodes well for a growing economy, but also impacts bond yields, as we will explain later.

The current administration is proposing a new stimulus bill of $1.9 billion, which would include checks for every American, additional unemployment money and more. With the Senate now in a Democratic majority this very well may pass and inject more money into consumers’ pockets. This may not be good for our country in the long run, but it will certainly put money into consumers pockets in the short run.

All of this points to a rebounding economy and suggests staying invested in equities, at least in the short term.

Remember that a recession is defined as two back-to-back quarters of lower GDP. Because of the reasons just described, this seems improbable in the next four to eight quarters. However, we may see a corporate tax increase that mutes the recovery somewhat, but spring follows winter.

Evenly Distributing Sector Weights

One of the adjustments we are making is that we are rebalancing our stock sector weightings. We believe that even if the market remains stable or flat, there could be significant

Source: Morningstar

movement within the market. The tech sector could face serious regulatory pressure, and if you pair that with tech stocks’ historically high valuations it isn’t hard to see how the sector could be vulnerable. On the other hand, other industries are likely at the beginning of a resurgence.

A case in point. Several months ago, our senior partner Scott Pinkerton needed his home air conditioner repaired. It took two months to get a part. What’s more, clients of ours who ordered boats and RVs are on a two-year back order!

There is pent-up demand. As last year’s laggers become leaders, their percentage market cap relative to others will rise. This will force the index funds to buy them, which will drive up their prices, which could create a positive virtuous upward cycle.

Finding Well-Priced Stocks

If you need income, dividends still matter—a lot. Fortunately, many of the higher-paying dividend companies are not overvalued and quite fairly priced. With rising interest rates and a growing economy, expect us to add more financials and industrials to our income-producing portfolios.

Energy stocks, often good dividend payers, have been in an oil slick for nearly a decade. However, as the economy comes back it is reasonable to believe that people will return to planes, trains, and automobiles. OPEC has been holding supply firm so this should benefit U.S.-based producers and refiners. However, President Biden has already revoked the permit for the Keystone XL Pipeline and is making aggressive moves to restrict leasing of federal lands for oil and gas drilling. It appears that instead of Joe from Scranton, a friend of frackers, he is environmental Joe.

If we do see inflation, selected real estate could do very well. Obviously, it is not time to load up on shopping mall operators, but cell tower, medical service and fulfillment centers have pricing power. Finally, there are still great companies in the consumer discretionary and health care sectors that are reasonably priced, have decent dividends and strong, steady growth.

Turning to High-Yield Municipal Bonds

Source: Bloomberg as of September 30, 2020.

We are re-examining our bond holdings due to historically low yield in treasuries and investment grade corporate bonds, as demonstrated in this chart from Standard and Poor’s. Where do we find tax advantaged or tax-free bonds with reasonable yield in a low interest rate environment?

We have focused on high-yield municipal bonds, which have a history of yielding as well as many other fixed income classes, as shown in this chart from Bloomberg and have a lower default rate.

Wolves We are Still Watching, even as we tend our crops.

- A Stock Market Bubble. The threat of wolves never goes away entirely, so we’re still watching. The biggest, scariest one? A stock market bubble. This wolf is always in the backs of our minds, but fortunately he (or she) isn’t at the fore of the pack. One common indicator of a bubble is valuations. The S&P 500 is currently trading at a premium P/E multiple. This means the market is expensive. Two things temper our concern: 1) the concentration of the market in large growth companies and 2) low returns on alternatives. The top 10 companies represent 28.6% of the market’s total capitalization. If you eliminate those 10 companies, the PE multiple drops from 22.3 to 19.7. Secondly, if you look at the earnings yield of bonds, comparatively stocks are reasonably priced.

- Volume of Small Options Trading. There are other baby wolves that howl every once in while, and recently one howled quite loudly when individual investors made GameStop’s stock skyrocket, forcing hedge funds that had shorted it to lose millions and causing the trading platform Robinhood and several others to temporarily limit trades of the stock. When everyone is a stock expert and day trading proliferates, many believe the end is near. It is true this is a sign of excess, but it can last for a long time without affecting the broader markets.

- Government Debt. In this chart we see the enormity of our U.S. government debt. Many believe that government debt doesn’t matter, while others are just tired of talking about it. Logically however, a government cannot borrow money endlessly and give it away without implications. Excess government debt historically leads to inflation—as illustrated by the photo of a Weimar Republic woman using German marks for kindling in a period of hyperinflation. We believe the strength of Bitcoin and gold is a hedge turned speculation against inflation and against the risk of owning flat currencies.

- Inflation, Interest and Quantitative Easing. Quantitative easing is a fairly new tool of the Federal Reserve in which they essentially print money to buy bonds. This can artificially push down interest rates. In 2010, a group of prominent economists sent an “open letter to the world” warning then-Fed chairman Ben Bernake that quantitative easing would devalue our currency. It didn’t happen. But that doesn’t mean it won’t.

Our new U.S. Treasury chair Janet Yellen is a self-proclaimed Keynesian, so we may expect more pressure on the Fed to do more. Note that the Fed has a stated goal of reflating the economy, so we achieve about 2 ½% inflation consistently. However, the economy is not a machine that the Fed can easily control. Why? Because of us. Our economy is driven in large part by our mindset and confidence. This may eventually make it difficult for the Fed to “stick the landing” on interest rates. If inflation reaches to 2.5% and keeps climbing, the Fed will have to raise rates. That will make our debt payments higher and our ability to manage our recovery more challenging. It will make our bonds less attractive.

In summary, we are anxious investors. We wake up reading and fearing what may go wrong. On the other hand, many retirements have been ruined when investors get shaken from their long-term plans because of wolves that are in the woods, but not on the doorstep—or when they don’t turn the crops when all of the indicators suggest they should. We believe our economy will continue to recover, producing positive returns for U.S. stocks. We also think bonds will continue to yield little, but most of us need them for security and diversity. Based on this we will turn our crops and continue to keep a close eye on the wolves.

Important Disclosures

FourThought Private Wealth is owned by FourThought Financial, LLC (FFLLC) is an SEC-registered investment advisor. For information pertaining to FFLLC please contact FourThought Private Wealth or refer to the SEC’s website, www.adviserinfo.sec.gov. This presentation is provided for informational purposes, not as personal investment advice. This presentation may contain certain forward-looking statements which indicate future possibilities. Any hypothetical example is intended for illustrative purposes only and does not represent an actual client or an actual client’s experience, but rather is meant to provide an example of the process and the methodology. Any reference to a market index is included for illustrative purposes. It should not be assumed that your account performance will correspond directly to any benchmark index. There is no guarantee views and opinions expressed herein will come to pass. Past performance is no guarantee of future results.