The Look of Recovery in a Post-Pandemic World

(To download a printable pdf of this white paper, click HERE).

Many of us have experienced it. You are driving to Florida and the kids can’t wait to see the Magic Kingdom. They have been marking the days on their calendars when you tuck them into bed. Finally you are on your way, and after an excruciatingly long drive you cross the Florida state line and pass the “Welcome to Florida” sign.  The kids go berserk. Then you tell them, “Kids, it is another four hours before we get to Disney.” These are the longest four hours of their lives. Kids can be impatient.

The kids go berserk. Then you tell them, “Kids, it is another four hours before we get to Disney.” These are the longest four hours of their lives. Kids can be impatient.

Investors can be impatient as well. Can you blame us? Sometimes things happen, we don’t act quickly enough, and we regret it. At other times we overreact and regret it. Welcome to our second quarter commentary on the economy: “Are We There Yet?” That’s the question everyone is asking, but what does “there” look like? Are we in a recovery? A bubble? An inflationary spiral?

We’re Coming Out of a Crisis but Don’t Yet Know the Long-Term Effects

It’s clear that we are recovering from the COVID crisis. However, we can’t yet comprehend the implications of this on the economy, society, education system, or even our personal health. We know that we are living in historic times and we are naturally anxious. Many feel that another shoe will drop. Are these feelings irrational or pointing to something below the surface?

At FourThought Private Wealth we see the economy recovering and believe the chance of a recession in the next year is highly unlikely. In our opinion, the stock market has fully priced in this reality and will not continue to grow as it has.

We are watching certain issues closely, such as geopolitical conflicts and the future threat of inflation. We are positioning our portfolios so we can identify these trends and shelter our investments. As we continue to travel down the highway, we see some important “billboards,” including stock market valuations, debt, inflation, speculation, and opportunities. Let’s examine each.

1. Is the Market Way Ahead of Itself?

Beware of pattern recognition bias. When we see a graph with trend lines, understand that our brains instantly search for patterns. We often find patterns in randomness. When you look at the chart below, note

Chart Source: FactSet, Standard & Poors, J.P. Morgan Asset Management. Guide to Markets – U.S. Data are as of March 31, 2021

that in 2000 and in 2007 the market topped near a certain level—yet now it has raced substantially higher. We get the uneasy feeling that the market is extended and getting way ahead of itself. Next, we look in the box and notice that the current PE of the market is 21.9x, which seems to be high relative to previous inflection points. These are rational and important observations.

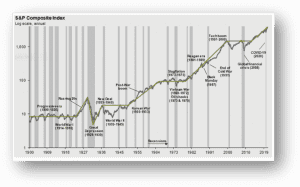

The second chart provides a different perspective of the markets since 1900. From this vantage point we can understand how the trend can prompt a completely different emotion. We see periods of

Chart Source: FactSet, Standard & Poors, J.P. Morgan Asset Management. Guide to Markets – U.S. Data are as of March 31, 2021

flatness followed by periods of growth. We are reminded that from 2000- 2012, the market went for years without eclipsing its previous highs.

2. Is the Market Overvalued?

The chart below shows the current price to earnings (PE) ratio of the market versus its historic average. It is

Chart Sources: FactSet, Standard & Poors, J.P. Morgan Asset Management. Guide to Markets – U.S. Data are as of March 31, 2021

important to think about these relative to inflation. If you have lower inflation, the markets can support higher prices.

A rule of thumb we use at FourThought is to take the market’s PE multiple and add the projected inflation rate. If the sum is less than 20, the market is attractive. The current forward PE of the S&P 500 is 21.88. This is based on forward expectations of earnings. Remember that companies often underestimate their earnings to protect against lawsuits for “misleading” analysts if they have an earnings miss.

Could these be understated? Eighty percent of the companies beat analysts’ expectations in the fourth quarter. If they are understated, then valuations are not abnormally high.

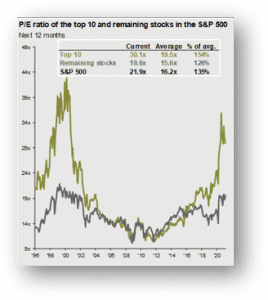

Another factor is the concentration of the market. We must look under the hood to better understand. The chart here segments the market between the largest ten companies in the S&P 500 and the other 490. The market’s forward PE ratio is above its historical average, but if you subtract the top ten companies this isn’t necessarily true.

Chart Sources: FactSet, Standard & Poors, J.P. Morgan Asset Management. Guide to Markets – U.S. Data are as of March 31, 2021

Our position is that the market isn’t cheap no matter how you slice it. From an investment perspective, now is the time to rebalance your portfolio and shift from overpriced companies to underpriced companies and sectors.

3. Is There Excess Speculation?

If you are driving down the highway with your family and you see a motorcycle popping a wheelie, giving you lewd hand signals and going 70 miles per hour, slow down. You could witness a wreck. No question, we are seeing excess speculation.

- A local developer stopped taking orders for new homes. He said he refused to take clients’ deposits when his company can’t deliver for over two years. They have a line of people willing to pay $20,000 to buy people out of their contracts.

- Friends recently sold their house. They had it listed for one day, had nine showings and 16 offers—all over the asking price.

- In a group chat between college friends, one friend taunted Scott to buy crypto currency because “only in crypto can you make this kind of money!”

- The saga of GameStop stock.

- The saga of Dogecoin—a crypto currency that people are only buying because it is going up.

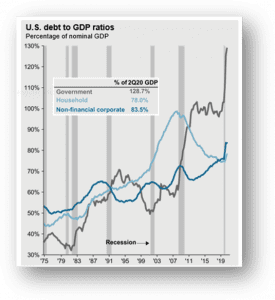

4. Has Our Debt Reached a Tipping Point?

Many people have great confidence that our government can pull the levers of the economy and steer us to safety. However, it’s a mistake to think the economy is like a machine that provides dependable inputs and predictable outputs. To a large extent management of the U.S. economy is a confidence game. It is important to remember that we don’t control what we think we control and that we are not gods.

There was a huge kerfuffle after the last global crisis about how much public debt was too much. Professors Carmen Reinhart and Kenneth Rogoff wrote a controversial paper that posited when a country’s economy reaches a public debt to GDP of 90%, their future growth slows. Their work ran into a replication problem and of course you have the issue of causation, but the premise has not been refuted. Our current debt to GDP is 107%.

Intuitively, most of us realize that you can’t borrow your way to prosperity and there is eventually a negative tipping point. Are we there yet?

Chart Sources: FactSet, Standard & Poors, J.P. Morgan Asset Management. Guide to Markets – U.S. Data are as of March 31, 2021

History teaches that debt does matter. First, the debt must be paid off. This is why Reinhardt and Rogoff found that it slows long-term growth. Simply put, we are borrowing tax revenue from the future to stimulate our economy today. This means that in the future our government will have to spend less than it takes in to pay off our debt. Stimulate today at the expense of de-stimulating tomorrow.

5. Will a Strong Economy Result in Inflation?

On our office lobby wall are some German marks from the Weimar Republic (remember wheelbarrows of money to buy a loaf of bread). Milton Friedman once said, “Inflation is always and everywhere a monetary phenomenon.” This means that if we increase the supply of dollars, which borrowing does, and we do not increase the supply of products, the cost of products will go up. This creates inflation and it hurts the poor. That being said, some countries that practiced austerity during the last crisis hurt themselves unnecessarily.

Fed Chairman J. Powell said on a 60 Minutes episode that aired on April 11 of this year that in the expansion of 2017-2019, the economy reached an unemployment level in the 3% range and workforce participation increased. Amazingly, this occurred without inflation. There were underlying forces at work, including the world’s aging population and the effect of technological improvements to productivity. In our view, these are allowing us to grow without inflation.

If we start to experience inflation that gets substantially above 2.5 % we believe the Fed will raise rates in an attempt to slow the economy. This could sow the seeds of a recession.

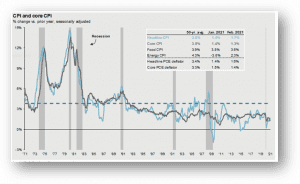

As you can see in the chart below, inflation is currently tame and well below its historical average. Some inflation is healthy; deflation is something we need to worry about. Think about Japan for the last 30 years—the Nikkei is still below its high in 1989!

Chart Sources: FactSet, Standard & Poors, J.P. Morgan Asset Management. Guide to Markets – U.S. Data are as of March 31, 2021

Is this time different? Different from what? The stagflation spiral of the ‘70s and ‘80s, or the recovery of 2009-2015? The answer of course is yes. We think we need to worry about the supply chain and wage push inflation.

6. Is Our Supply Chain Really Compromised?

Our supply chain is a mess. We are experiencing something many of us have not seen in our

Chart Source: FactSet

lifetimes: a shortage of goods and services. There are empty shelves in stores and a shortage of truck drivers making it worse. This may be temporary, but it could lead to big cost increases.

7. Is Inflation Pushing Wages Up?

Many restauranteurs are reporting that they are having a hard time finding workers. In a close-to-home example, one FourThought client owns a business in an industrial park. There are 14 businesses in the park, and on a recent visit we counted “help wanted” signs in the windows of ten of them. Low unemployment should lead to higher wages, and wages are the biggest expense in the costs of goods and services. Rising wages could result in higher inflation—again, potentially causing the Fed to raise rates.

We know the principles of supply and demand in the economy. Demand shortages can be partially addressed though stimulation (classic Keynesian economics). But when we have lack of supply, we require different economic solutions (see Frederick Van Hyack). Some believe our recent government stimulus is a Keynesian solution to a supply side problem. Fed Chair Powell disagrees.

To summarize the situation, markets are expensive but the economy is in a recovery, our government is borrowing and stimulating like no other country in the history of the world, and we don’t yet see substantial and sustainable inflationary pressures. Prices are high, but in our opinion not in bubble territory. To put it another way, we still have growth and low inflation.

We believe we are in a long-term bull market that has a way to run but could be in danger of correcting. Our strategy is to pull into the slow lane and proceed with caution. We must not let the heavy traffic tempt us to change our destination.

Our base case is that we will see a temporary spike in inflation as our economy adjusts but we will continue to be in a low inflation environment. There are certain companies and industries we believe will continue to grow well above average, including alternative energy, cloud-based technology, cyber security, luxury goods, warehousing, global payments, and online gaming. Read on to learn why we believe in these sectors.

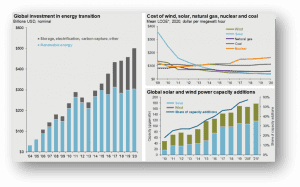

ALTERNATIVE ENERGY

The sources from which our world gets energy are changing. As shown in the graph here, wind and solar are now cheaper, per megawatt hour, than traditional carbon like coal, oil, and natural gas. This is good news for our environment and great news for investors.

NextEra Energy and Xcel Energy are electric utilities that are building solar and wind supplies and are two of our favorite companies in this sector. Xcel has received approval to invest $24 billion between now and 2025 to transform itself into a renewable energy leader. The political risk is low, and they have a strong, well-covered 2.5% dividend. Power generation is increasingly turning to zero-carbon sources which are quickly becoming the most efficient and lowest-cost source of new electricity throughout the U.S. (including the costs of energy storage).

Chart Source: FactSet, Standard & Poors, J.P. Morgan Asset Management. Guide to Markets – U.S. Data are as of March 31, 2021

Xcel operates in some of the most advantageous geography on the planet for the ongoing energy transition. The company operates in six of the 12 states comprising the American wind corridor, which is a patch of land that runs from West Texas to North Dakota and is home to roughly 70% of North America’s onshore wind capacity.

Xcel’s move toward wind has led to impressive cost savings for customers as the average monthly residential bill has decreased from 2013 ($84) to 2019 ($80). The company has decreased its exposure to energy prices while still enabling the business to grow its rate base, which is the core metric used by regulators to determine rate increases.

CYBERSECURITY

Cybercrime is a huge problem in today’s society. That is why we believe the move toward the cloud (think Salesforce, Microsoft Teams, AI etc.) will continue to create demand for products focused on securing the cloud. If the recent breaches and hacks have taught us anything, it’s that the bad guys online are constantly adapting. Just this April, the data of more than 500 million LinkedIn users was compromised.

Hackers are coming up with more sophisticated attacks. Existing endpoint protection and firewall solutions have not kept pace. Many organizations now have multiple (10 or more) different cybersecurity vendors who are all providing solutions that are still not enough to effectively protect them against the constant attacks taking place every day.

In other words, vendors are adding more and more locks to the front door, but that just forces the hackers through the unlocked windows.

However, some companies such as CrowdStrike (along with others such as Palo Alto Networks, FireEye, VMWare) are developing innovative solutions to this complicated problem. CrowdStrike’s cloud-based intelligence platform can proactively detect malware signatures and then immediately secure and protect all customers simultaneously from being impacted by them. This approach offers more effective protection from increasingly complex threats. It’s also a more cost-effective overall solution.

LUXURY GOODS

One of our long-term observations is that luxury goods companies have experienced strong, consistent earnings and revenue growth. Emerging wealth in Asia seems to be driving this phenomenon. Portfolio companies like Louis Vuitton and Nike are taking advantage of their cachet, quality, and brands to drive impressive long-term results. In our opinion this trend is durable and worthy of investment.

WAREHOUSE/SUPPLY CHAIN

The supply chain is changing. There is a need for redundancy because of the shortages experienced during the pandemic. There is also a push to domesticate the supply chain. For decades the driving decision has been for lower prices which drove production overseas. During the pandemic it became evident that countries will quickly nationalize production of key materials and products for the benefit of their constituents. The global supply chain has added risk. We believe that companies will accept higher prices in return for supply assurance and favor quality U.S. industrial companies to take advantage of this trend.

Other beneficiaries of the changing supply chain will be railroads, trucking and warehouse companies. We favor Prologis (warehouses) to participate in this trend.

ONLINE GAMING

Online gaming is a core, long-term trend that we believe is under appreciated. In 2020, the global gaming industry reached a revenue milestone of over $180 million. This exceeded the 2019 revenues of the global film industry by over $80 million.

(For in-depth information on the gaming industry, ask for our in-depth analysis and white paper or find it in the Resource Library on FourThought.com).

Gaming appeals to several generations, with the “average” gamer at approximately 38 years of age. The wide appeal of gaming has made it the dominant disruptor of the entertainment industry. It has changed the way we consume media and interact with others on a day-to-day basis.

We like many companies that have exposure to the gaming industry such as Nintendo, Activision, Sea Ltd, Tencent, Sony, and Microsoft.

In Summary

As we cross the border from pandemic to recovery our kids ask, “Mommy, Daddy, are we there yet?” We smile, look in the mirror and tell them we are getting close and it’s going to be great. We turn our attention to the road, proceed with caution and confidence. We are going to get there. We are going to be okay.

Important Disclosures

FourThought Financial, LLC (FFLLC) is an SEC-registered investment advisor. For information pertaining to FFLLC please contact FourThought Private Wealth or refer to the SEC’s website, www.adviserinfo.sec.gov. This presentation is provided for informational purposes, not as personal investment advice. This presentation may contain certain forward-looking statements which indicate future possibilities. Any hypothetical example is intended for illustrative purposes only and does not represent an actual client or an actual client’s experience, but rather is meant to provide an example of the process and the methodology. Any reference to a market index is included for illustrative purposes. It should not be assumed that your account performance will correspond directly to any benchmark index. There is no guarantee views and opinions expressed herein will come to pass. Past performance is no guarantee of future results.